Real Estate and Property Tax Strategies: Maximizing Deductions, Credits, and Savings

This comprehensive guide explores essential tax strategies for real estate owners and investors. Learn how to leverage mortgage interest deductions, navigate property tax limitations including the SALT deduction cap of $10,000, and capitalize on energy-efficient home improvement credits like the 30% solar panel installation credit and rebates up to $14,000. Understand how these elements impact your overall tax liability, reduce your tax burden, and enhance financial returns while ensuring compliance with IRS regulations.

Real estate ownership and investment offer significant tax advantages that can dramatically reduce your annual tax liability. By understanding and applying key tax strategies, homeowners and investors can capitalize on deductions for mortgage interest, navigate property tax considerations, and leverage credits for energy-efficient improvements. This guide provides a detailed examination of these strategies, incorporating specific data such as the $10,000 SALT deduction limit and energy credits covering 30% of solar panel installation costs and rebates up to $14,000. Whether you're a first-time homebuyer or a seasoned investor, these insights will help you optimize your tax position and enhance financial outcomes.

Mortgage Interest Deductions: Maximizing Tax Benefits

Mortgage interest deductions remain one of the most valuable tax benefits for homeowners. Under current IRS rules, taxpayers can deduct interest paid on mortgages up to $750,000 for primary and secondary residences. This deduction applies to acquisition debt used to buy, build, or substantially improve a qualified home. For properties purchased before December 16, 2017, the limit is $1 million. To claim this deduction, itemize on Schedule A of Form 1040, and ensure you receive Form 1098 from your lender detailing the interest paid. Strategic planning, such as refinancing to lower rates while maintaining deductible interest, can amplify savings. Note that interest on home equity loans or lines of credit is only deductible if used for home improvements, per IRS guidelines.

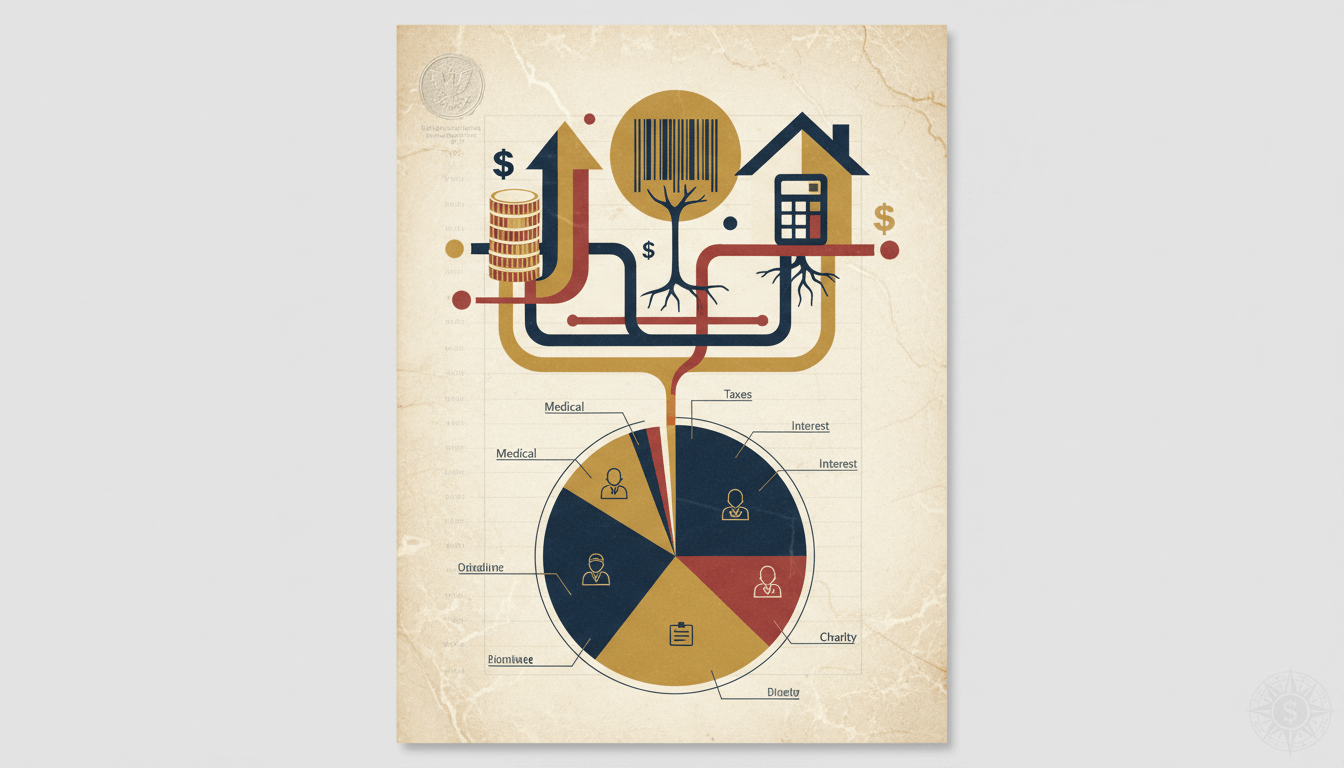

Property Tax Considerations and SALT Deduction Limits

Property taxes are generally deductible, but the Tax Cuts and Jobs Act of 2017 imposed a $10,000 cap on state and local tax (SALT) deductions, which includes property, income, and sales taxes. This limit applies to both single filers and married couples filing jointly, significantly impacting homeowners in high-tax states. For example, if your property taxes are $8,000 and state income taxes are $7,000, only $10,000 total is deductible. To mitigate this, consider bundling property tax payments in years when you expect higher itemized deductions or exploring local payment plans. Additionally, real estate investors can deduct property taxes as business expenses on Schedule E,不受SALT cap restrictions, providing an advantage for rental properties.

Energy-Efficient Home Improvement Credits and Rebates

The federal government offers substantial credits for energy-efficient home improvements to promote sustainability and reduce carbon footprints. Key incentives include a 30% tax credit for solar panel installation costs, with no upper limit, available through the Residential Clean Energy Credit. This credit applies to systems placed in service by 2034 and phases down thereafter. Additionally, rebates of up to $14,000 are available for other qualifying improvements like insulation, energy-efficient windows, and heat pumps under programs such as the Home Energy Rebates. These benefits not only lower your tax bill but also reduce utility costs over time. To qualify, ensure improvements meet ENERGY STAR standards and keep detailed records of expenses and certifications for IRS verification.

Integrating Real Estate Strategies into Overall Tax Planning

Effective tax planning requires integrating real estate strategies with your overall financial picture. For investors, depreciation deductions under MACRS (Modified Accelerated Cost Recovery System) allow you to deduct the cost of rental property over 27.5 years for residential real estate, reducing taxable income. Losses from real estate activities may be deductible under passive activity rules, with limitations based on income and participation. Homeowners should time property tax payments and mortgage refinancing to maximize itemized deductions in high-income years. Consult a tax professional to assess how these strategies interact with other deductions, credits, and tax brackets, ensuring compliance and optimizing long-term wealth accumulation.

Key Takeaways

Mortgage interest deductions can reduce taxable income for loans up to $750,000, with higher limits for pre-2017 acquisitions.

The SALT deduction cap of $10,000 limits property and other state/local tax deductions, affecting homeowners in high-tax areas.

Energy-efficient credits include 30% for solar panels and rebates up to $14,000, offering dual tax and utility savings.

Real estate investors can deduct property taxes as business expenses,不受SALT cap restrictions.

Strategic timing of payments and improvements aligns with overall tax planning to maximize benefits and ensure IRS compliance.

Frequently Asked Questions

What is the current limit for mortgage interest deductions?

For mortgages taken out after December 15, 2017, the deduction applies to interest on up to $750,000 of acquisition debt for primary and secondary homes. Pre-2017 mortgages have a $1 million limit.

How does the SALT deduction cap affect property taxes?

The SALT deduction caps total state and local tax deductions at $10,000 annually, including property taxes. This means if your property taxes exceed this amount combined with other SALT payments, the excess is not deductible.

Are energy-efficient credits available for rental properties?

Yes, rental property owners can claim energy credits for qualifying improvements, such as solar panels, but they must be used for the property and meet specific IRS criteria for business use.

Can I deduct property taxes if I don't itemize deductions?

No, property tax deductions require itemizing on Schedule A. If you take the standard deduction, you cannot separately deduct property taxes.

Conclusion

Real estate and property tax strategies provide powerful tools for reducing tax liability and enhancing financial security. By leveraging mortgage interest deductions, understanding SALT cap implications, and utilizing energy-efficient credits, homeowners and investors can achieve significant savings. Always maintain accurate records, stay informed about tax law changes, and consult with financial advisors to tailor these strategies to your unique situation. Implementing these approaches not only supports compliance but also fosters long-term wealth growth and sustainability.